Multiply your

QSBS exclusion

QSBS trust stacking lets eligible founders multiply the $15M per-taxpayer Section 1202 exclusion across properly structured non-grantor trusts — turning one exclusion into several.

GAIN EXCLUSION MATH

$15 Million

The federal QSBS gain exclusion per taxpayer, per issuer (stock issued after July 4, 2025 under OBBBA).

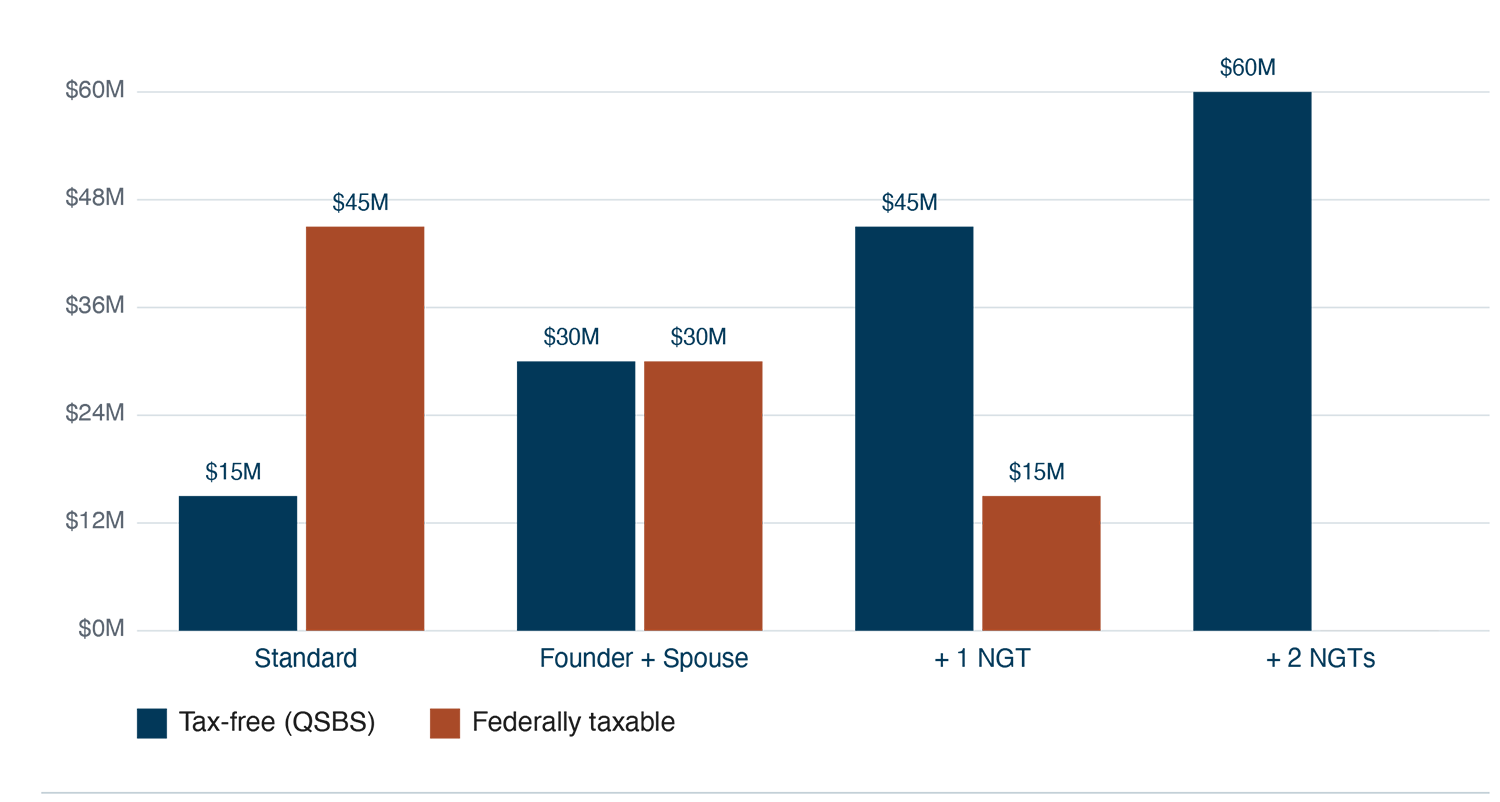

$60 Million

Founder/Investor + spouse + two non-grantor trusts. Four taxpayers.

Same exit. Same equity. Very different return to the family.

FIGURE 1 — FEDERAL GAIN SHELTERED ON A $60M EXIT

Stacked bars showing how the $60M moves from federally taxable into the QSBS-exclusion column as you add non-grantor trust taxpayers.

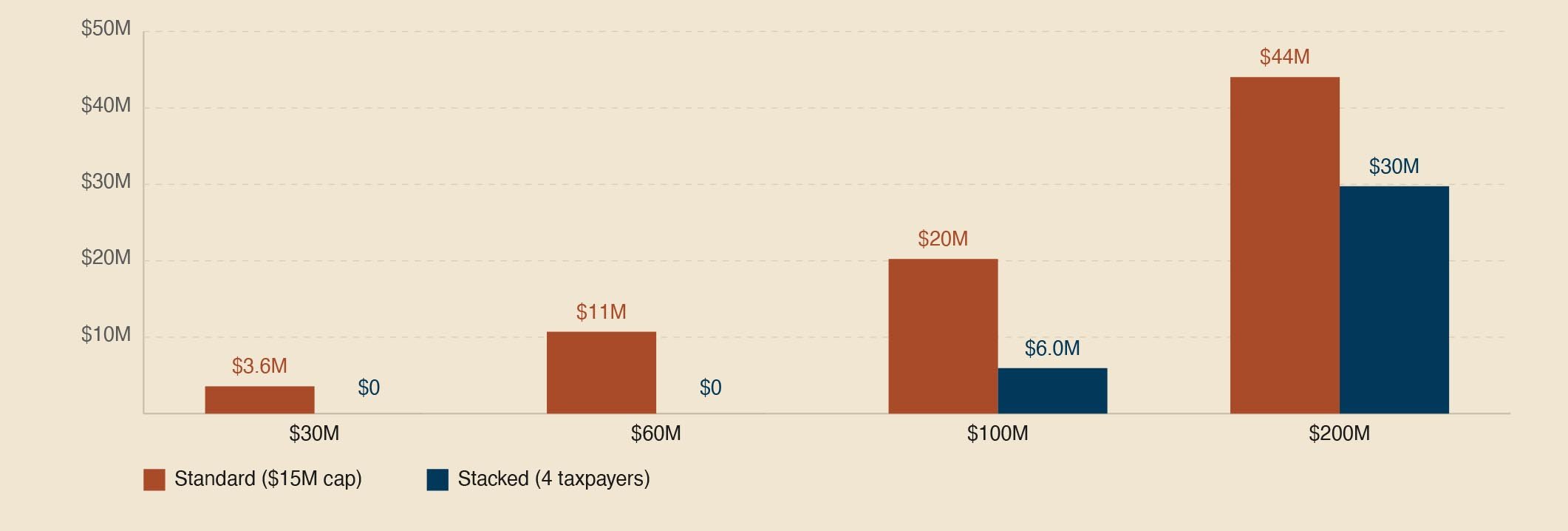

FIGURE 2 — FEDERAL TAX OWED AT EXIT

On a $200M exit, a four-taxpayer stack may shelter roughly $14M more in federal tax than a single taxpayer — same exit, same equity.

Take the Intake Quiz

2 minutes, no email required. The Intake Quiz takes your equity and family situation and recommends a structure. The fastest way to know whether this page applies to you.

Run your own facts.

Run your own numbers. Book a consult and we’ll model your exact equity and family situation in a personalized Promissory illustration.

HOW THE STRATEGY WORKS (4 STEPS)

Identify

Confirm eligibility and model the stack against the founder's cap table.

Transfer

Gift qualifying stock well before a liquidity event. Gifting inside 12 months of a signed LOI is a no-go zone —recharacterization risk spikes.

Design

Choose the right structures. SLATs (grantor) do NOT stack; SLANTs, NGTs, non-grantor IDGTs do.

Realize

At exit, each properly structured trust claims its own §1202 exclusion.

Dogpatch brings the advisory relationship. Promissory brings the trust infrastructure — drafting, valuation, and administration.

Who qualifies for QSBS trust stacking

Domestic C-corporation issuing the stock.

Most VC-backed software, hardware, biotech, climate companies qualify.

Gross assets under $75M at original issuance (post-OBBBA).

Five-year holding period for the full 100% exclusion (50% at 3 years, 75% at 4 years under OBBBA).

12–24+ months of runway pre-liquidity. Inside 12 months is a no-go zone.

Best fit: Seed through Series B. Series C possible with the right timeline.

On the live page, founders pre-screen against these chips visually, then jump into the Intake Quiz for a structured assessment.

FAQ’s

-

QSBS trust stacking is the practice of allocating qualifying Section 1202 stock across multiple eligible taxpayers — typically the founder, spouse, and one or more properly structured non-grantor trusts — so each can claim its own $15M federal exclusion at exit. It’s mainstream §1202 planning when done early, and risky inside 12 months of an LOI.

-

Planning should begin 18–24 months before a likely liquidity event. Inside 12 months, recharacterization risk rises sharply, and after a signed LOI the window is effectively closed for new structures.

-

No — California does not conform to federal §1202 and continues to tax the gain at ordinary state rates. QSBS trust stacking is a federal benefit; California outcomes depend on trust situs, beneficiary residency, and source rules.

-

No — Dogpatch coordinates with your existing CPA and attorney rather than replacing them. Promissory’s panel attorneys handle the trust drafting, with sign-off pathways for your own counsel.

-

Promissory’s platform fee is a transparent $7,500 standard package covering up to four trusts, attorney review, valuation, and tax-form prep, plus $1,500/yr trust custody after year one. The Dogpatch advisory overlay is scoped after the initial consult.

-

No — properly structured QSBS trust stacking is recognized §1202 planning that venture-backed founders have used for two decades. Real trusts, real beneficiaries, real administration, real holding periods. We turn down fact patterns that don’t support it.

DISCLAIMER

Educational only. Not tax or legal advice. Tax outcomes depend on individual facts and circumstances and may vary. Any potential tax savings discussed are illustrative and not guaranteed. California does not conform to federal QSBS treatment. Dogpatch Wealth coordinates with your CPA and attorney; we do not replace them. Services provided in partnership with Promissory